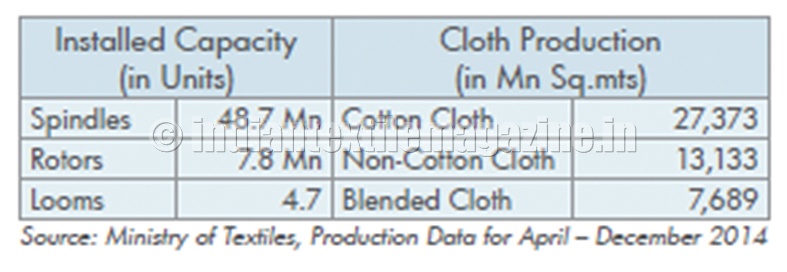

Currently India is the second largest textile manufacturer in the world with its manufacturing base comprising 24 per cent of the global installed spindle capacity and eight per cent of the installed rotor capacity. The textile sector employs over 45 million people directly and indirectly, making it the second largest employer after agriculture.

India textile industry

After going through one of the worst phases in the last quarter of FY14 and in the initial quarters of FY15, when local and overseas demand declined, the sector is now expecting overall demand to pick up soon based on the following encouraging factors:

• The textile industry to benefit from the “Make in India” campaign unveiled by the Government.

• Exports set to increase in the coming years as Indian textile mills prepare themselves to fill the gap created due to lower exports by Chinese mills.

• Exports to be more broad-based by raising the number of export destinations, as against the current concentration on a few Western economies.

• Domestic demand to strengthen in the coming quarters, in line with the expected improvement in economic growth.

• Mechanization levels in the sector to witness an improvement as more and more mills opt to strengthen their manufacturing infrastructure to improve efficiency.

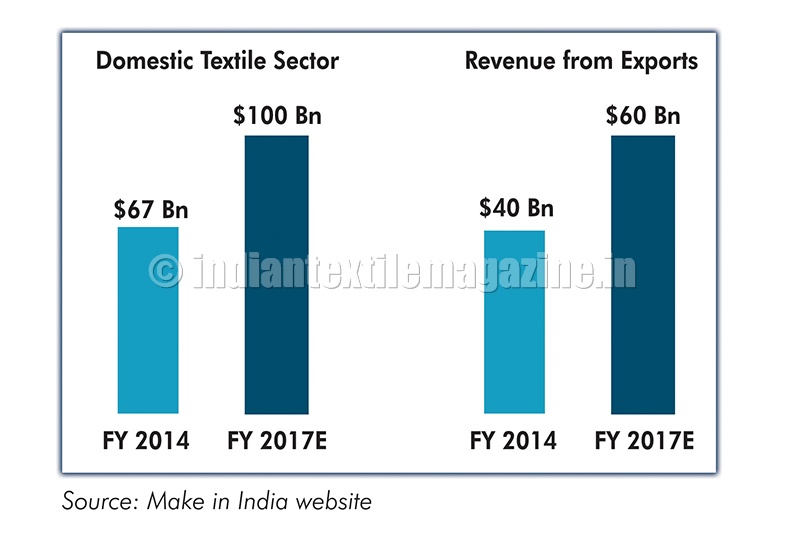

The ‘Make in India’ campaign outlined by the Government is aimed at strengthening the manufacturing base in the country. Its inclusion in the program would immensely benefit the textile sector as the government undertakes sector-specific initiatives and implements policies and programs to improve overall business climate and investments. This measure is expected to attract private investments into all segments of the textile industry, from yarn processing to textile finishing. In addition, export promotion measures would help the sector achieve its stated goal of $300 billion worth of exports by 2024-25.

Exports would strengthen on the back of revival of demand in the traditional markets and penetration into new geographies. Consumer demand for textiles products in the US market is expected to strengthen in the coming quarters as US economic growth is seen to be stabilizing. Since it is the largest export market, its revival would improve textile exports from India.

To lower dependency on the US and European markets, the Modi Government is taking measures to encourage textile exporters to explore alternate markets in Latin America and Asia. Though initially exports to these markets would be minimal they may pick up as the consumption pattern in the emerging markets in Latin America and Asia is changing.

Textile exports from China are expected to slow down in the coming years, presenting an opportunity for Indian mills to increase their market share in international markets. Increasing labour cost in China is eroding the competitive advantage enjoyed by Chinese mills in the international textile market, presenting an opportunity to Indian mills that are currently the second largest exporters of textile products. In addition, the decision by Chinese mills to move up the value chain from exports of basic textile products to value-added items is expected to benefit Indian textile manufacturers.

Domestic demand for textile products is set to recover owing to the improving economic scenario. Pick-up in industrial activity, improvement in business sentiment in key service sector industries like IT-BPM, softening of inflation and cut in interest rate are all expected to improve economic growth in the coming quarters. The resultant revival in domestic consumer demand would help improve the overall textile consumption in the country.

Higher demand for textile products in the coming quarters, as a result of developments outlined above, would push up the capacity utilization ratio in Indian textile industry. This and the continued increase in consumer demand as the economy improves would prompt textile mills to embark on capacity expansion. Consequently, capital expenditure in the textile industry would positively revive.

Growing investments

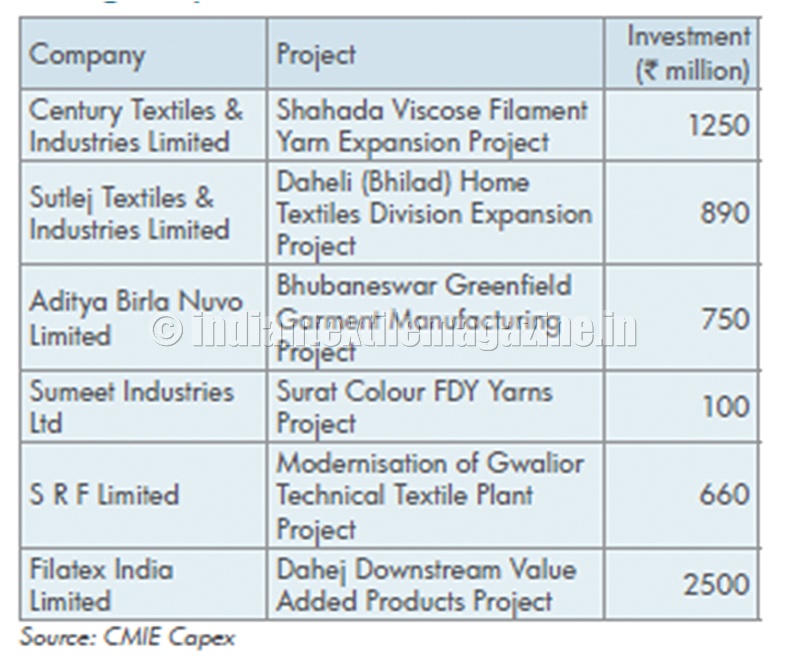

Capital investments in the textile sector are reviving with projects worth hundreds of crores announced in the past six months. Several of these projects are scheduled to come online over the next couple of years, adding capacity in the sector when consumer demand is expected to fully revive. Announcement of these mega projects is a reflection of improving confidence among textile mills about the prospect of demand revival in the coming years.

Major capital investment projects announced during the past 6 months

Challenges facing the sector

In the international market, Indian textile exports face tough competition from Pakistan, Bangladesh, Vietnam and Cambodia. Favorable tariff measures enjoyed by these countries in European markets have directly impacted textile exports from India. While Indian textile exporters have to pay high duty on exports to European markets, exports from Pakistan, Bangladesh and Cambodia are duty free. Since European countries form the second largest export destination after the US, losing out market share in this region would negatively impact the industry.

In addition to growing competition in European markets, Indian mills, especially cotton yarn manufacturers, face the prospect of lower yarn demand from China, one of the largest markets. In 2014, the Chinese Government introduced a new cotton policy that encourages textile mills in the country to consume locally produced cotton and yarn in place of imports. This policy shift has lowered the overall cotton and cotton yarn imports made by Chinese mills. As Indian cotton yarn manufacturers have a high level of exposure to Chinese textile mills, this policy shift has its adverse impact. With the policy unlikely to be rolled back, Indian yarn producers will have to penetrate on newer export markets.